The construction industry, and its broader ecosystem, erects buildings, infrastructure, and industrial structures that are the foundation of our economies and are essential to our daily lives. It has successfully delivered ever more challenging projects, from undersea tunnels to skyscrapers. However, the industry also has performed unsatisfactorily in many regards for an extended period of time. The COVID-19 pandemic may be yet another crisis that wreaks havoc on an industry that tends to be particularly vulnerable to economic cycles.

External market factors, combined with fragmented and complex industry dynamics and an overall aversion to risk, have made change both difficult and slow. The COVID-19 crisis looks set to dramatically accelerate the ecosystem’s disruption that started well before the crisis. In such times, it is more important than ever for actors to find a guiding star for what the next normal will look like in the aftermath and make the bold, strategic decisions to emerge as a winner.

Video

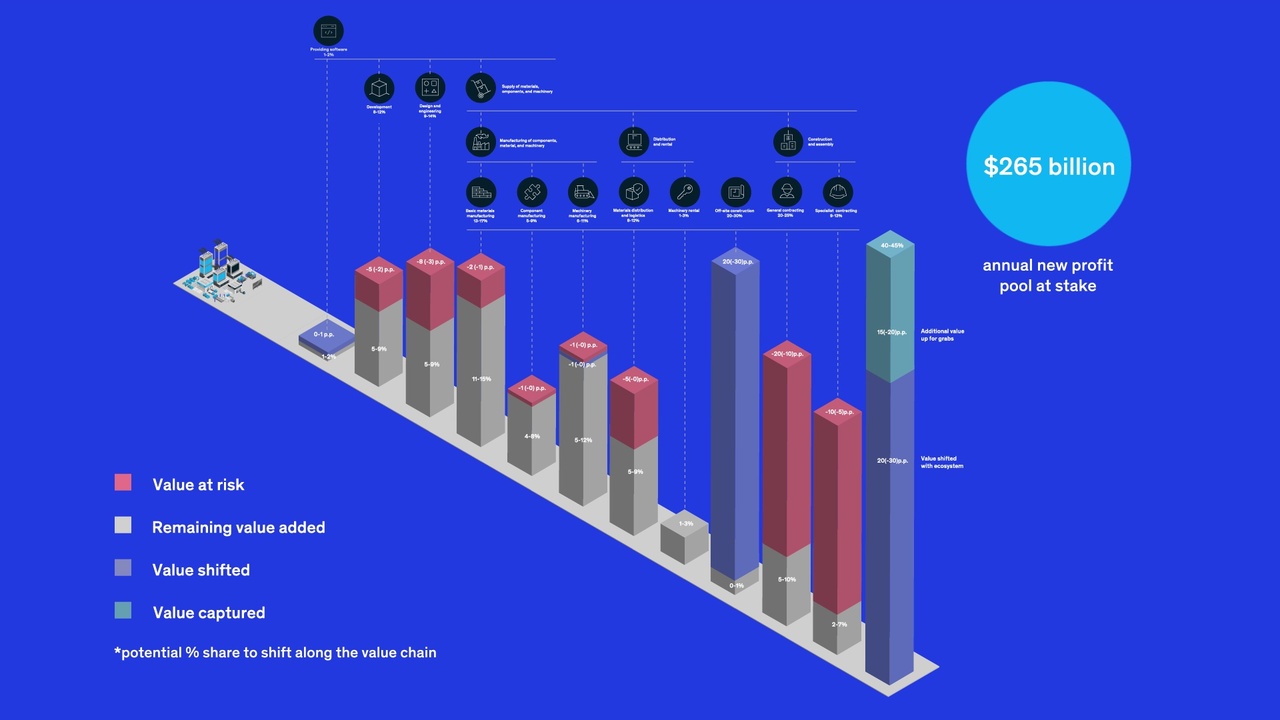

Nine shifts are expected to disrupt the construction industry ecosystem. Where could the effects be felt along the value chain?

Many studies have examined individual trends such as modular construction and sustainability. This report provides an assessment of how the full array of disruptive trends will combine to reshape the industry in earnest. Our research builds future scenarios based on more than 100 conversations with experts and executives, firsthand experience serving clients throughout the ecosystem, and reviews of other industries and their transformation journeys. We confirmed the trends and scenarios that surfaced by conducting a survey of 400 global industry leaders. Finally, we quantitatively modeled value and profit pools across the value chain, based on company data today, and formulated future scenarios. We found overwhelming evidence that disruption will touch all parts of the industry and that it has already begun at scale.

Would you like to learn more about our Capital Projects & Infrastructure Practice?

Among our findings are the following:

- Construction is the biggest industry in the world, and yet, even outside of crises, it is not performing well. The ecosystem represents 13 percent of global GDP, but construction has seen a meager productivity growth of 1 percent annually for the past two decades. Time and cost overruns are the norm, and overall earnings before interest and taxes (EBIT) are only around 5 percent despite the presence of significant risk in the industry.

- Nine shifts will radically change the way construction projects are delivered—and similar industries have already undergone many of the shifts. A combination of sustainability requirements, cost pressure, skills scarcity, new materials, industrial approaches, digitalization, and a new breed of player looks set to transform the value chain. The shifts ahead include productization and specialization, increased value-chain control, and greater customer- centricity and branding. Consolidation and internationalization will create the scale needed to allow higher levels of investment in digitalization, R&D and equipment, and sustainability as well as human capital.

- The COVID-19 crisis will accelerate change that has already started to occur at scale. Our research suggests that the industry will look radically different five to ten years from now. More than 75 percent of respondents to our executive survey agreed that the nine shifts are likely to occur, and more than 60 percent believe they are likely to occur at scale in the next five years. We already see concrete signs of change: for example, the permanent modular- construction market share of new North American real-estate construction projects has grown by 50 percent from 2015 to 2018, R&D spending among the top 2,500 construction companies globally has risen by approximately 77 percent since 2013, and a new breed of player has emerged to lead the change. Two-thirds of survey respondents believe that COVID-19 will lead to an acceleration of the transformation, and half have already raised investment in that regard.

- A $265 billion annual profit pool awaits disrupters. A value chain delivering approximately $11 trillion of global value added and $1.5 trillion of global profit pools looks set for overhaul. In a scenario based on analysis and expert interviews by asset class, strongly affected segments could have a staggering 40 to 45 percent of incumbent value added at risk, even when the economic fallout from COVID-19 abates—value that could shift to new activities such as off- site manufacturing, to customer surplus, or to new sources of profit. If the value at stake is captured by players in the construction ecosystem, total profit pools could nearly double, from the current 5 to 10 percent.1 The scale and pace of change and the appropriate response will differ greatly among real-estate, infrastructure, and industrial construction—but all of them will be affected. Players that move fast and manage to radically outperform their competitors could grab the lion’s share of the $265 billion in new and shifting profits and see valuations more akin to those of Silicon Valley start-ups than traditional construction firms.

- To survive and thrive, incumbents must respond. All of the players in the construction value chain will need to develop their strategies for dealing with or leading disruption. This is especially true for engineering and design, materials distribution and logistics, general contracting, and specialized subcontracting, all of which are likely to face commoditization and declining shares of value for parts of their activities. Companies can try to defend their positions and adjust to the changing environment, or reinvent themselves to take advantage of changes in the industry. All will need to invest in enablers like agile organizations.

- Investors are well advised to use foresight on the respective shifts in their investment activity and will have ample opportunity to generate alpha. Policy makers should help the industry become more productive and achieve better housing and infrastructure outcomes for citizens. And owners stand to benefit from better structures at lower cost if they play their part in making the shifts happen.