Leader in McKinsey's Private Equity and Financial Services Practices working with private equity, fintechs, payments, and technology clients with a focus on value creation, strategy, M&A and growth topics

The past two decades have seen enormous growth in payments systems. Twenty years ago, contactless cards, mobile payments, and digital wallets were in their infancy. Today, they are ubiquitous. But as new payments systems continue to emerge, only a few are likely to survive in the long run. Of more than 200 systems introduced between 1993 and 2000, for instance, only PayPal emerged as a standout success.

What does it take to create a retail payments offering with staying power? It’s a billion-dollar question with a fundamentally simple two-part answer: large-scale access to stores of value so that senders and receivers can exchange funds, plus a trusted operator that routes transactions between counterparties and enforces fair governance standards. However, the first of these requirements has historically made launching a new scheme difficult for all but incumbents that already manage checking accounts and credit lines. This competitive “moat” has been strengthened by network effects. Incumbents also benefit from the “last inch” problem in retail: how to enable a buyer to transfer their payments credentials to a merchant. Incumbents control physical point-of-sale (POS) devices, and extending them to other payments methods is a slow and costly process.

Yet the future may offer brighter prospects for new payments systems. A host of structural changes over the past few years may lead to many barriers to entry coming down:

Customers are congregating in ecosystems and marketplaces where they consume similar services and can be more easily accessed, like Amazon, Alibaba, and Uber

Technological advances are enabling companies to quickly scale up new products across critical masses of senders and recipients, creating large seed populations in digital marketplaces, social networks, and other groups

Application programming interfaces (APIs) are enabling payments to be easily integrated with other products via underlying bank rails such as automated clearing house (ACH) payments and wire transfers

Higher digital spending is allowing new “plug and play” solutions to be adopted without the need to roll out physical POS devices.

These changes have triggered a proliferation in new consumer-to-merchant payments networks and schemes over the past decade. New aspirants in developing countries—such as Alipay and WeChat in China, Paytm in India, and MercadoPago in Argentina—are leapfrogging physical card infrastructure. Tech companies are capitalizing on their consumer reach to establish intermediaries between card networks and consumers in the form of Apple Pay, Google Pay, Grabpay, and others. Card networks are diversifying their offerings via M&A, with Visa acquiring Earthport and Plaid and MasterCard acquiring Vocalink and Nets. Meanwhile, countries are quickly establishing new domestic standards of usage via ventures such as MobilePay in Denmark and Swish in Sweden.

Networks and schemes: What’s the difference?

As payments providers broaden their horizons, it is helpful to clarify terms: “network” and “scheme” are often used interchangeably, but strictly speaking, they refer to different things:

A network, at its simplest, is a directory of participants along with the information required to access their stores of value and settle transfers: names and addresses, account details, and so on. Primary networks, such as ACH and real-time gross settlement (RTGS), are integrated with bank systems and do not rely on any other settlement mechanisms to execute payments.

A scheme also has a directory of participants, but what differentiates it from a network is that it also enforces rules and standards. As well as connecting to bank networks to transfer funds, it ensures that participants abide by rules and standards on fraud liability, participant eligibility, data security, and other matters. Some “pure” schemes, such as the National Automated Clearing House Association (NACHA) in the US, focus only on managing their own rules and standards without maintaining a directory of participants. Examples of payments schemes include Visa, Mastercard, JCB, Amex, Girocard, China UnionPay, Zelle, and TransferWise.

Hybrid schemes typically connect to both schemes and networks. They often include a store of value (that is, some kind of deposit account) and overlay their own rules to create a common set of standards. Examples of hybrids include Alipay, WeChat Pay, PayPal, and Twint.

How to start a payments system in 2020

Building a new payments system is no longer the exclusive preserve of financial institutions. Companies with strong ecosystems can take advantage of them to set up networks and schemes with their customers, suppliers, or other third parties. Incumbents, meanwhile, are venturing into new territories. Card schemes have used acquisitions to expand into networks and schemes catering to business-to-business (B2B), cross-border, and POS lending, while banks have invested in domestic debit networks and digital payments.

For entrants and incumbents alike, a new network or scheme can be scaled up by following the approach outlined below.

Identify an internal or external seed population with a critical mass of senders and receivers that generates strong network effects for its members. With an internal population, the company builds on a customer base or marketplace of its own that currently uses other schemes to send and receive payments. With an external population, the company partners or targets an external entity with a growing or under-served population, develops scheme standards, and then acquires customers. Companies with payments systems at this stage include the ride-sharing app Uber, the US restaurant-delivery services GrubHub and Caviar, and the US education, healthcare, and travel payments platform Flywire.

Collect payments information and enable internal payments. Since direct-to-account payments methods are typically cheaper than card schemes, collecting payments information is financially advantageous. It is also getting easier, thanks to innovations such as Plaid for accessing bank accounts and API-based open-banking standards. Providers can enable internal payments within a target population before extending the scheme to external users. Amazon, which collects bank-account information to enable direct ACH transactions, exemplifies this stage of a payments system.

Define pricing, rules, and standards. Graduating from a network to a scheme involves enforcing rules and standards for participants. (Swish, a mobile payments scheme in Sweden, has reached this stage in its evolution.) Branding is one key decision point: will the scheme have a different brand from the parent company? Will accepting merchants be required to communicate or display their acceptance? Another set of choices relates to open-data standards and access: what information is transmitted with each transaction? What data is retained, for how long, and who stores it? What data do participants and third parties have access to? Then there is pricing: what price is applied to transactions versus dollar flows? Does it vary by underlying payments type? Do cross-border transactions incur additional fees? Finally, fraud liability rules must be determined: if an unauthorized user gains access to a member’s credentials and conducts a fraudulent transaction, does that member have any recourse? If so, who is liable for that amount, under what conditions?

Create access channels and expand distribution. Opening up a payments system to participants beyond the seed population requires new access points for different purposes. One is onboarding: allowing new participants to join the network and collecting their payments information. Another is APIs access, to extend acceptance of the system via proprietary or third-party distribution channels. Yet another is dedicated marketing and sales, to expand the teams that drive acceptance. Finally, third-party channel access is needed to enable the system provider to work with regional acquirers to bundle a scheme as part of their merchant-acceptance packages. Payments systems that have reached this stage include PayPal, which offers payments via buttons embedded in e-commerce sites, and Alipay, which has expanded acceptance via its 2018 partnership with First Data (now Fiserv).

Is it worth it?

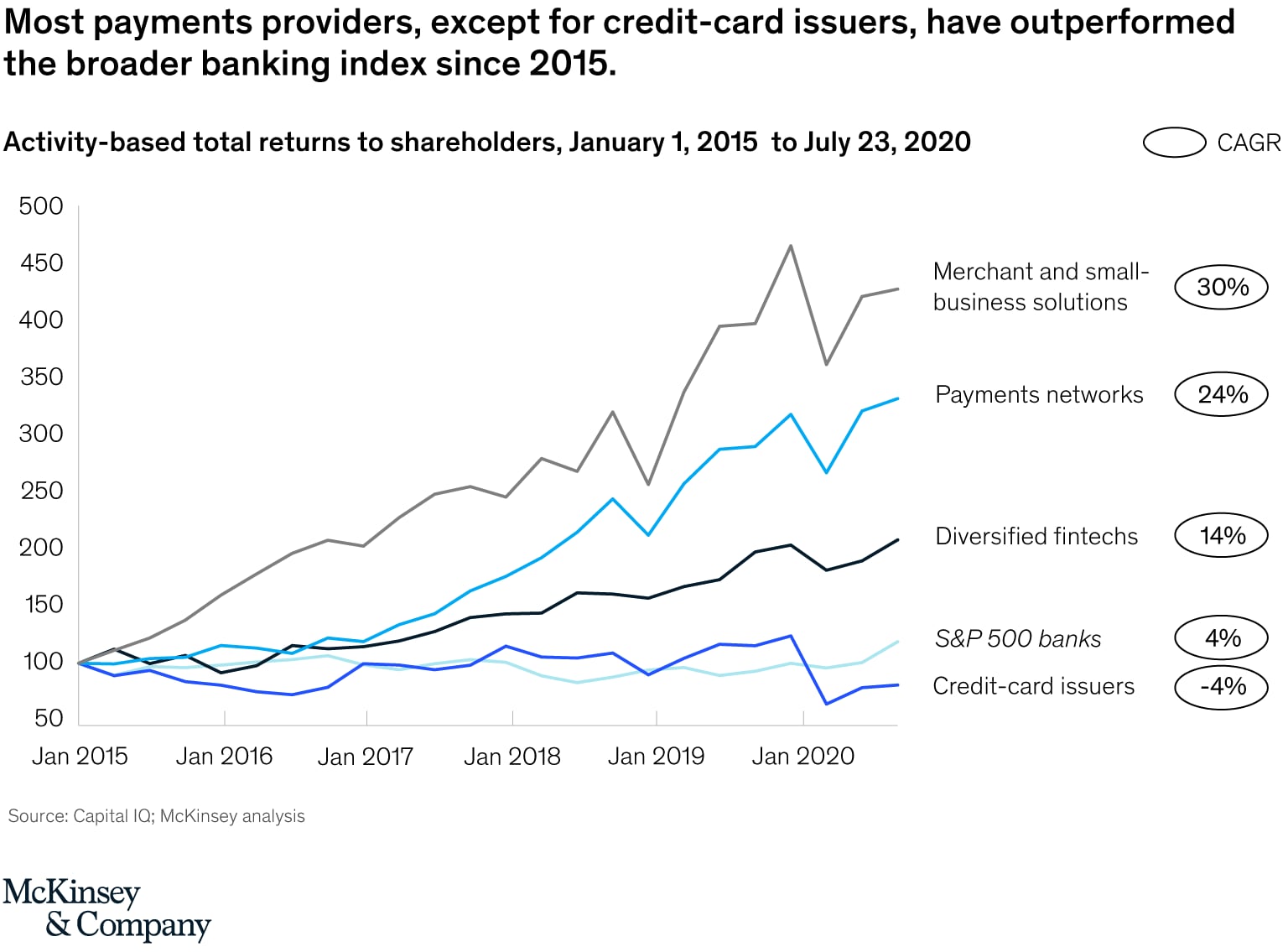

Successful payments systems have generated high returns in recent years (Exhibit 1). The returns of payments players (24 to 30 percent) have been multiples higher than fintechs, banks, and credit card issuers (-4 to 14 percent).

Throughout history, as payments evolved from barter to coins to notes to cards to digital wallets, the underlying revenue model for each method (whether merchant, interchange, or flat fees) has remained much the same. However, as digital payments methods, omnichannel, and instant payments converge to transform the payments industry, revenue models are likely to change, too. New networks and schemes will aggregate volumes and build ecosystems that generate network effects, enabling them to maintain premium pricing for customers while using low-cost bank rails to transfer funds. For instance, systems offering POS capabilities typically charge merchants 2.5 to 3 percent of transaction value, while paying considerably lower wholesale rates on the back end.

The outlook for incumbents

For payments providers of all kinds, the implications of these developments could be far-reaching. Levels of disruption are likely to vary for different players in the incumbent value chain.

Banks face a broad strategic question: should they manage their own payments networks or have third parties manage them—which could create strategic dependency? Banks in small to mid-size markets that lack the scale to justify investing in new payments networks could instead form regional agreements to aggregate scale and work with third parties to manage technology infrastructure, while retaining strategic and economic control of new schemes. Banks in larger markets with the scale to operate their own networks will need sufficient market share to create a coalition that sets standards for the new scheme, like the large US banks that created Zelle and opened it up to other banks.

In all markets, launching a new payments method calls for caution in pricing. If banks capture too much economic value, they could antagonize regulators and attract new entrants capable of underpricing them. Other options banks could consider include improving existing networks and connecting national debit schemes across regional markets.

Global schemes are continuing to explore new ways to capture volume, such as investing in linkages to bank accounts. Visa’s $5.3 billion acquisition of Plaid—a maker of APIs that allow companies to easily execute bank-account payments—is a striking example of the kind of expansive move that global schemes are increasingly pursuing. Meanwhile, Mastercard has made significant investments focused on B2B payments, as seen in its acquisition of Transfast, SessionM, as well as Nets’ account-to-account payments business.

Another option for global schemes is to establish co-acceptance partnerships. Examples include Visa’s partnership with Tencent to gain access to the WeChat Pay network in China and PayPal’s deal with Google Pay to increase POS acceptance.

Acquirers can differentiate themselves and add value for merchants by becoming a one-stop shop for an expanding array of payments schemes. Conversely, confining themselves to one or two schemes could put them at risk of disintermediation should these schemes decide to go directly to merchants. Acquirers can also offer merchants value-added services such as fraud analytics and merchant lending and help them upgrade their capabilities for additional schemes such as Alipay and WeChat Pay.

Opportunities for new entrants

Operators of new networks and schemes can create value for participants by increasing their reach, delivering a superior experience, and reducing their operating costs.

In terms of reach, tailoring a new network or scheme to meet the needs of its intended users through customized governance, rules, and pricing enables operators to maximize the pool of participants. When it comes to user experience, in the payments business, the experience often is the product. Consider the latest generation of POS devices or the introduction of Apple Pay and Google Debit. Years ago, the introduction of payments schemes like Paypal and Venmo enabled users to move money more easily via fewer steps than with previous systems. New networks and schemes can do the same by tightly integrating the payments experience into their own regional marketplaces and ecosystems.

Finally, new networks and schemes are free from the legacy infrastructure costs that large global networks bear. This, combined with purpose-built design, allows operators to pass on cost savings to participants. If those participants perceive real value in broader reach, better experience, and operating cost savings, operators can quickly monetize their offering. They can do this both directly, through transaction fees, lending, and pricing, and indirectly, through customer “stickiness” and increased brand reach and value.

Now may be the moment for incumbent providers to expand into new niches with specific needs, and for other ecosystems to control their destiny by building their own payments networks and schemes. Though incumbents will face threats, the growth of payments methods looks set to continue, presenting opportunities for incumbents and disruptors alike.