The decade from 2010 to 2020 marked a period of relative calm for the US healthcare industry, with national health expenditures (NHE) rising at predictably steady rates. Then the COVID-19 pandemic unleashed a prolonged period of disruption, illness, and loss that continues to wane slowly. Yet, even now, there is no rest for the weary. A gathering storm arising from labor shortages, inflation, and endemic COVID-19 challenges the industry anew. It threatens affordability and access to care for consumers, and it poses material risks to profitability for providers, payers, and other healthcare stakeholders. McKinsey research reveals the combined effects of these forces could accelerate the increase in NHE by approximately $600 billion through 2027.

Deep dive about the gathering storm in US healthcare

In our Gathering Storm four-article series, we address:

The uncertain future of US healthcare

What are the major storm clouds on the horizon, and how does the potential impact compare to past periods of upheaval?

The transformative impact of inflation on the healthcare sector

How does rising inflation—both broadly, and specifically, as the industry confronts a clinical staff shortage—affect access, costs, and growth?

The affordability challenge of endemic COVID-19

What impact might an endemic COVID-19 have on the expected trajectory of healthcare costs

An opportunity to reorder the healthcare industry

What should stakeholders do about the gathering storm

How healthcare leaders choose to respond will make all the difference. In 2018, in advance of an NFL playoff game, then-New England Patriots quarterback Tom Brady posted an unattributed quote on social media: “Fate whispers to the warrior, ‘You cannot withstand the storm.’ The warrior whispers back, ‘I am the storm.’”

Healthcare leaders, especially those in the private sector, have an opportunity to step up and invest in innovation for the betterment of healthcare. Indeed, implementing a well-known set of interventions—in care delivery transformation, administrative simplification, clinical productivity, and technology enablement—could generate a collective opportunity of more than $1 trillion and potentially up to $1.5 trillion through 2027, according to McKinsey analysis. However, to move fast enough to capture this opportunity, healthcare leaders need to rethink how they approach organizational growth and transformation.

Those who act now could set themselves apart in leading transformative improvements of healthcare and accrue a sustainable competitive advantage for their organizations. McKinsey’s 15th annual healthcare conference, held in July 2022 in Chicago, explored the current healthcare climate, forces contributing to the coming storm, and steps healthcare leaders can take to help them weather these turbulent times and thrive.

Theme one: New forces affecting the healthcare industry

The highest inflation levels since the 1970s, the growing likelihood of a recession, and low consumer sentiment are buffeting the US economy—and the healthcare industry is not immune to their effects. Workforce spending, which accounts for more than 40 percent of total spending for healthcare providers is rising rapidly. 1 And endemic COVID-19 may bring increased morbidity, especially for the most vulnerable segments of the population.

The unprecedented scale and scope of the pandemic may skew our ability to use history as a guide, but a look at previous responses to periods of inflation and economic downturns may provide helpful reminders of what could lie ahead and how industry leaders can respond.

Healthcare inflation

Healthcare inflation is being driven primarily by rising labor costs, but other factors are exacerbating cost pressures. 2 For example, costs for supply inputs have grown 15 to 25 percent over the past three years. Overall, by 2027, inflation could result in an additional $370 billion in healthcare spending above the expected baseline increase. 3

Labor shortages

The healthcare labor crisis spans job categories, but McKinsey research—both globally and in the United States—reveals it is especially acute in nursing. 4 A decline in labor pools from outside the United States, demographic shifts, and increased turnover driven by healthcare worker decisions to pursue non-patient-care careers or to retire are intensifying pressure on labor supply. Although turnover rates show signs of abating from pandemic highs, the United States may confront a shortage of 200,000 to 450,000 registered nurses and 50,000 to 80,000 physicians by 2025 as demand for care rises and supply lags. Reversing this trend will require health systems to take a multipronged approach to recruiting, retaining, and retooling their workforces, and to meet the needs of their frontline workers effectively and compassionately.

COVID-19’s ongoing impact

It now appears likely that COVID-19 will be with us for years to come, affecting the overall health, economy, and public healthcare workforces of the United States. 5 Endemic COVID-19—with an estimated 100 million annual cases—could translate to an additional $222 billion in healthcare spending by 2027. 6 This includes spending associated with acute care (primarily hospitalizations), long COVID, and ongoing vaccinations and testing. Furthermore, endemic COVID will likely create ongoing challenges for those struggling with chronic conditions and mental health issues. This will be coupled with accelerated demand for behavioral health services above the annual baseline spending growth rate of 2.5 percent, which is likely for years to come. 7

Theme two: Who will bear the burden?

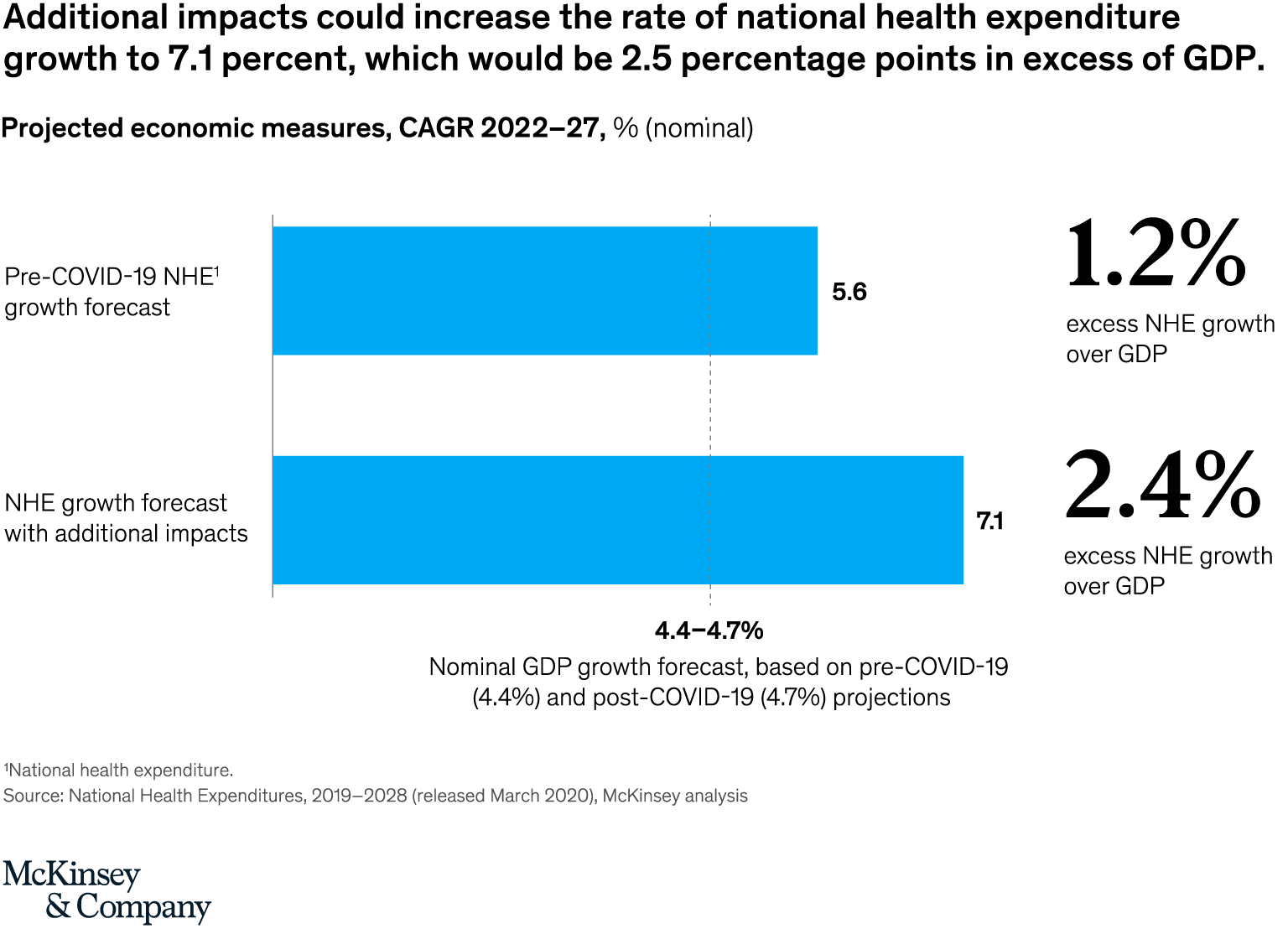

Without the effects of the brewing storm, NHE was expected to grow at a rate of 5.5 percent per year through 2027. 8 These additional costs, however, are projected to push up the rate of NHE growth to 6.8 percent according to McKinsey analysis, or about 2.5 percentage points above forecasted GDP growth (Exhibit 1). The gap could be even larger if the economy faces an extended recession. Who will bear this additional impact? McKinsey modeled three scenarios to explore the spending burden through the lens of employers, consumers, and government.

Exhibit 1

Employers

In a survey of employers, 60 percent of respondents reported healthcare cost increases that outpaced inflation in the past three years; 63 percent expect that trend to continue, signaling potential cost challenges in the future. Moreover, 95 percent of employers stated they would pass along any cost increases greater than 4 percent per annum to employees. 9 High-deductible health plans (HDHPs) have been a leading avenue for employers to pass along costs to their employees (Exhibit 2). In 2021, 32 percent of employers surveyed offered an HDHP, and they reported that 28 percent of their employees have enrolled in one. This continued shift in costs has left employees on the hook for an increasingly large portion of the employer-sponsored health insurance expenses, with lower-income families disproportionately affected. According to the Petersen-KFF Health System Tracker, employees enrolled in employer-sponsored plans spend an average of 4 percent of their family income on health insurance premiums and out-of-pocket expenses combined; however, for those in families with incomes at 199 percent of federal poverty levels and below, the average payment jumps to 104 percent of family income. 10

Exhibit 2

Consumers

While average household savings remain temporarily high due to the pandemic, consumer confidence is dropping, and real wage growth is negative as a result of inflation. 11 Consumers already face substantial exposure to medical expenses—in a February 2022 survey, for example, more than 20 percent of consumers reported having more than $1,000 in medical debt—and they will have difficulty absorbing these higher costs for much longer. 12 In an earlier survey, 35 percent of respondents who had deferred care reported they had done so due to a lack of affordability. 13 Notably, individuals covered by employer-sponsored insurance report the lowest overall satisfaction with their coverage.

Government

A range of factors indicate that it may be difficult for the government to absorb the additional medical-cost burden. First, recent record-high federal budget deficits have brought the federal debt to historic highs. 14 The two largest deficits in history occurred in 2020 and 2021 at $3.1 trillion and $2.8 trillion, respectively. 15 This spending has increased the federal debt as a share of GDP to 124 percent. 16 Meanwhile, rising interest rates are increasing federal-debt service costs. Additionally, healthcare spending represents a record 20 percent of GDP. 17 The Medicare trust fund is projected to reach insolvency in 2028 if action is not taken, even accounting for the 2 percent sequestration cuts 18 which resumed effect in July. 19 Policy makers can explore a wide range of interventions to help ensure the United States gets sufficient value from increased medical costs, starting with better health outcomes.

Exhibit 3

Theme three: How to weather the storm

During the pandemic, leaders across the entire healthcare ecosystem rallied in surge after surge around the highest priorities, collaborated in unprecedented ways, and made and executed decisions at a breakneck pace—all to save lives and pull the health system back from the precipice. Now they can build on that momentum to not only weather the storm but also emerge stronger. Although profit pools are at risk, healthcare leaders who adjust their business models accordingly can expect bright prospects for their organizations in the years ahead. 20

Accelerating and scaling innovation in care delivery transformation, productivity improvement, technology enablement, and organizational growth will be central to healthcare leaders’ efforts. Together, investing in these areas could create value of more than $1 trillion and up to $1.5 trillion (Exhibit 4). 21 Attaining this value will require structural shifts to the system to better align incentives among risk bearers and deliver a patient-centric experience along the entire care continuum.

Exhibit 4Care delivery transformation

The future of care delivery is fundamentally changing. 22 We are slowly but steadily moving to a world in which care delivery is more personalized and supported by technology. More patients receive care in ambulatory settings, at home, and virtually. Data and analytics inform decision making across the care continuum. The shift to value-based care is reflected in care models and insurance. Private investors increasingly fund all of these changes in care delivery. Meanwhile, regulatory shifts support increased price transparency and secure sharing of patient data, and the healthcare ecosystem overall, while still fragmented, is becoming more integrated.

Improve clinical productivity and simplify administrative operations

Compared to most other industries, healthcare lags in productivity improvement. In fact, labor productivity has actually declined: between 2001 and 2016, the healthcare industry contributed 9 percent of US economic growth and 29 percent of job growth. 23 On average, clinical activity accounts for 75 percent of healthcare system costs; 24 administrative activity incurs the remaining 25 percent. 25 Healthcare systems need not wait for policy makers or regulators to institute top-down changes to improve productivity in both areas. Rather, leaders can improve clinical productivity in the short term by integrating several small solutions into a single platform—for example, to support a discharge planning tool in an acute-care setting or an asset optimization tool in a surgical center—that makes it seamless for clinicians to use.

On the administrative side, the bulk of costs come from customer service activities, and disproportionately from issue resolution rather than value-added services. 26 Healthcare systems could streamline these activities and make them more customer-friendly across touchpoints. Financial transactions associated with claims, premiums, and payments are the second-highest cost category; they thus warrant targeted productivity improvement efforts to unlock.

Technology enablement

During the pandemic, when providers and payers pivoted to tech-enabled care delivery, they discovered that they have the capacity to redesign systems much more quickly than they previously thought possible. Now they can continue to invest in technology enablement—a prerequisite for success in a value-based, full-risk environment. Moreover, $250 billion of US healthcare spending could potentially shift to virtual or virtually enabled care, which may support two primary objectives of value-based care: lowering cost of care and improving outcomes. 27 Likewise, proactive levers aimed at preventive health and chronic-condition management and initiatives to reduce waste and fraud are well suited to tech enablement. Although much of the promise of tech enablement—for example, truly personalized care, improved clinical decision making, and predictive decision making—is still aspirational, only those who roll up their sleeves can hope to realize the value.

Organizational growth and transformation

In economic downturns, the most resilient organizations (roughly the top quintile across industries including healthcare) exhibit special traits. 28 They accelerate decision making and have a bias toward action. They pursue a disciplined approach to growth rather than simply retrench to weather the storm. They invest disproportionately in areas that will drive growth or provide the greatest return. They double down on efficiency by prioritizing initiatives to make step changes in productivity, and they work to strengthen their balance sheet. They also make strategic portfolio moves—including divestitures, mergers, and acquisitions—timed first to the downturn and then the recovery. In return, these organizations—dubbed “resilients”—achieved approximately 100 basis points of excess total returns to shareholders compared to non-resilients during recovery and acceleration post-downturn.

***

The current wave of economic, operational, and health challenges buffeting the healthcare industry would test the mettle of even the most resolute leaders. But with much at stake, now is the time for leaders to thoughtfully and tirelessly implement the interventions that can sustain them in the near term and improve the industry for years to come.