| This week, battery storage gets even more versatile, and a McKinsey on China podcast explores opportunities amid slower growth. Plus, we resurface a terrific 2007 interview with strategy expert Richard Rumelt, in which he describes how Steve Jobs took a successful “predatory leap.” |

|

|

|

| What’s more exciting than battery storage? If you said “a lot,” you’ve been missing out on the market’s breakneck, if somewhat stealth, expansion over the past few years. |

| Here are some basics: an energy-storage device stores energy for later use. Obvious enough. It can power electric and hybrid vehicles, as well as billions of smartphones and other electronics. And then there are batteries as big as shipping containers. These guys aren’t holding volts for your emergency flashlight; they power data centers, hospitals, universities, hotels, restaurants, retail stores, and more. And they’ve got a particularly neat trick, which is they store energy when prices are low and release it when they are high. Exciting, indeed. |

| Storage can be deployed both on the grid and at an individual’s home or business. A complex technology, its economics are shaped by a variety of factors: customer type, location, grid needs, regulations, customer load shape, rate structure, and nature of application. Recently, some local utilities have established programs to pay residential energy-storage owners for feeding power from their batteries to the grid during peak demand periods. In return, customers receive compensation, such as a credit on their utility bill. As electric utilities grapple with systemic shifts, especially changes to rate structures, energy storage will also come into play. |

| The implications are big for the electric-vehicle market, which was slow to take off because charging stations were too few and far between. Now battery storage is changing that. And it’s making waves in the power sector. With prices dropping faster than anyone expected—battery-pack costs were recently $230 per kilowatt-hour, down from $1,000—battery storage is playing a bigger role in energy markets, moving from niche uses like grid balancing to broader ones such as replacing conventional power generators for reliability, providing power-quality services, and supporting renewables integration. And as the rise of renewables—solar and wind—continues, so will the need to store all that decarbonized electricity. |

| Cost has been plummeting for a few reasons: global demand for consumer electronics and electric vehicles spurred investments in battery-pack manufacturing. Other hardware such as inverters, containers, and climate-control equipment also got cheaper, thanks to design advances and efficiency gains in manufacturing and supply-chain management. |

| And “soft” costs (customer acquisition, permitting, and interconnection, among others), have dropped too. Experts forecast costs will fall another 50 to 70 percent by 2025, meaning players in the market, from storage developers to system integrators, should move fast. |

|

|

|

| OFF THE CHARTS |

| Can we not talk about Brexit for a sec? |

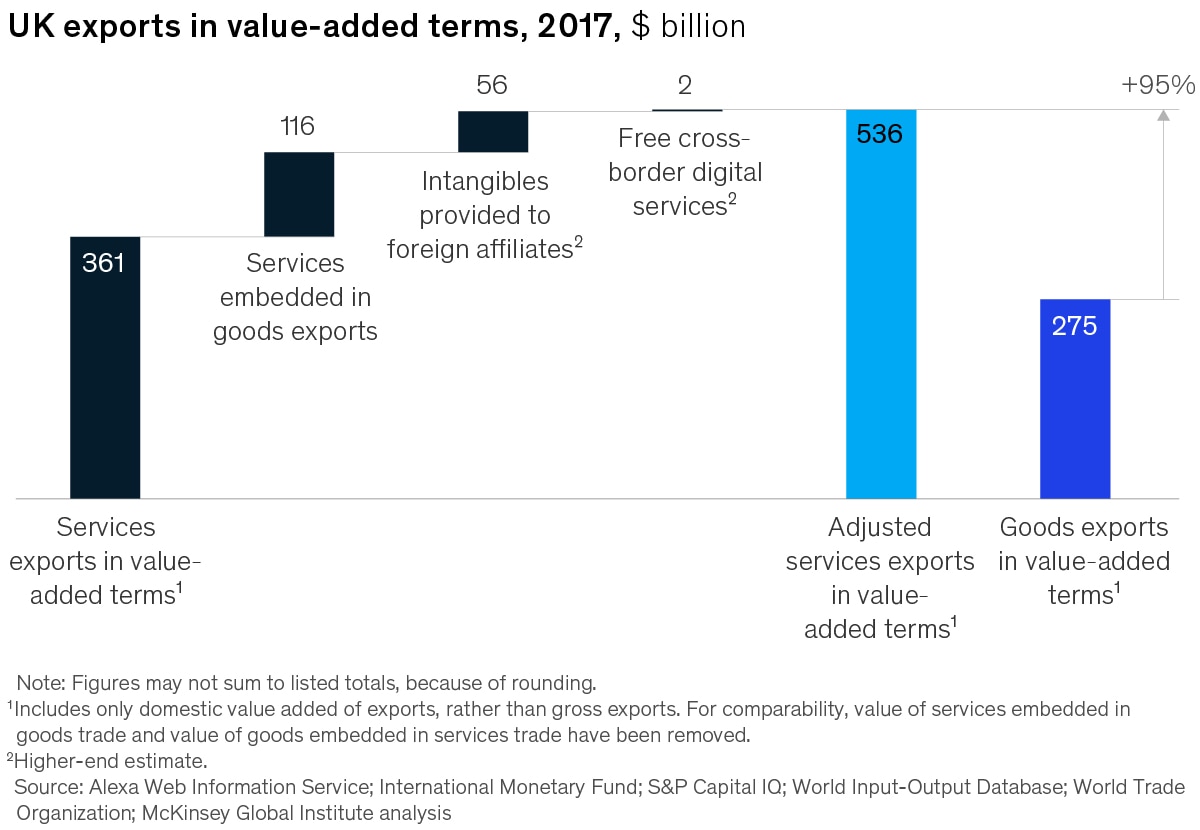

| No matter how Brexit eventually ends up, it’s important to take a longer view of trade and exports, critical engines of the United Kingdom’s economy. Right now, services exports are almost twice the value of the country’s goods exports in value-added terms. But UK businesses must seize new opportunities in the fast-growing services and digital trades to sharpen their international competitiveness. |

|

|

|

|

|

|

| MORE ON MCKINSEY.COM |

| Try conducting a premortem | After a project team is briefed on a proposed plan, its members imagine the plan has failed. This prompts everyone to anticipate threats and hurdles, and what may have begun as blind support can give way to creative problem solving. |

| Of ‘superstars’ and strategies | Today’s superstar phenomenon—the growing concentration of economic success by large companies, cities, and even sectors—has implications for business leaders around the world. Here’s what every CEO needs to know. |

| The ever-changing store | Many retailers believe—rightly—that format redesign is often too risky, takes too long, and costs too much. Agile can help. |

|

|

|

|

|

| THREE QUESTIONS FOR

|

| Richard P. Rumelt |

| In 2007, the McKinsey Quarterly interviewed Richard P. Rumelt, professor at UCLA’s Anderson School of Management and renowned strategy expert. Here are three questions from that interview, in which he offered insights into strategic thinking that remain timely today.

|

|

|

|

|

| Many executives have told us they feel that they are wasting a lot of time on strategic planning. What advice would you give them? |

| Most corporate strategic plans have little to do with strategy. They are simply three-year or five-year rolling resource budgets and some sort of market-share projection. Calling this strategic planning creates false expectations that the exercise will somehow produce a coherent strategy. These resource budgets simply cannot deliver what senior managers want: a pathway to substantially higher performance. |

| There are only two ways to get that. One, you can invent your way to success. Unfortunately, you can’t count on that. The second path is to exploit some change in your environment—in technology, consumer tastes, laws, resource prices, or competitive behavior—and ride that change with quickness and skill. This second path is how most successful companies make it. |

| Lots of people think the solution to the strategic-planning problem is to inject more strategy into the annual process. But I disagree. I think the annual rolling resource budget should be separate from strategy work. My basic recommendation is to do two things: avoid the label “strategic plan”—call those budgets “long-term resource plans”—and start a separate, nonannual, opportunity-driven process for strategy work. |

| How does a company position itself to take advantage of change? |

| Back in the mid-1990s I was researching strategy in the global electronics industry. I interviewed 20 to 30 executives, CEOs, and division managers and asked fairly simple questions. Which company was the leader in their market? How did that company become the leader? What’s their own company’s strategy? |

| I saw an interesting pattern. Most executives easily explained how companies became market leaders: some sort of window of opportunity opened, and the leader was the company that was the first to successfully jump through that window. Not exactly the first mover but the first to get it right. |

| But when I asked these same executives about their own strategies, I heard a lot about doorknob polishing. They were doing 360-degree feedback, forming alliances, outsourcing, cutting costs, and so on. None of them even mentioned taking a good position quickly when the industry changes.

|

| Then in 1998 I had the chance to talk with Steve Jobs after he’d come back and turned Apple around. “Steve,” I said, “this turnaround at Apple has been impressive. But everything we know about the personal-computer business says that Apple will always have a small niche position. So what are you trying to do? What’s the longer-term strategy?” |

| He didn’t agree or disagree with my assessment. He just smiled and said, “I am going to wait for the next big thing.” Jobs didn’t give me a doorknob-polishing answer. He was waiting until the right moment for that predatory leap, which for him was Pixar and then, in an even bigger way, the iPod. That predatory approach of leaping through the window of opportunity and staying focused on those big wins—not on maintenance activities—is what distinguishes a real entrepreneurial strategy. |

| How do we know which changes are important? |

| That’s a very tough question. It is a key issue—the next frontier. And it is under-researched, under-written about, and under-understood. I call it “strategy dynamics.” |

| Most of the strategy concepts in use today are static. They explain the stability and sustainability of competitive advantages. Strategy concepts like core competencies, experience curves, market share, entry barriers, scale, corporate culture, and even the idea of “superior resources” are essentially static, telling us why a particular position is defensible—why it holds the high ground. |

| If the terrain never changed, that would be the end of the story. High ground is always high, and low ground is always low. But in business, unlike geology, change happens in years rather than millennia. In the modern business world, there are earthquakes all the time that quickly take the low ground and raise it high and, at the same time, submerge some mountain peaks below water. |

| Strategy dynamics studies how those changes would shift each dimension of an industry. Would the industry become more concentrated or less? More integrated or less? Would there be more product differentiation or less? More segmentation or less? Given consumer desires and available technologies, how should the industry or business look in, say, ten years? Where are the economic forces trying to take you? Should your strategy ride those forces or fight them? |

|

|

|

| BACKTALK |

| Have feedback or other ideas? We’d love to hear from you. |

|

|

|

|

|

Copyright © 2019 | McKinsey & Company, 55 East 52nd Street, New York, New York 10022

|

|

|

|