| This week, we provide business leaders with a perspective on the evolving coronavirus outbreak. Plus, ten trends the fashion industry should consider in these uncertain times, and Kevin Sneader, McKinsey’s global managing partner, talks business in 60 seconds. |

|

|

|

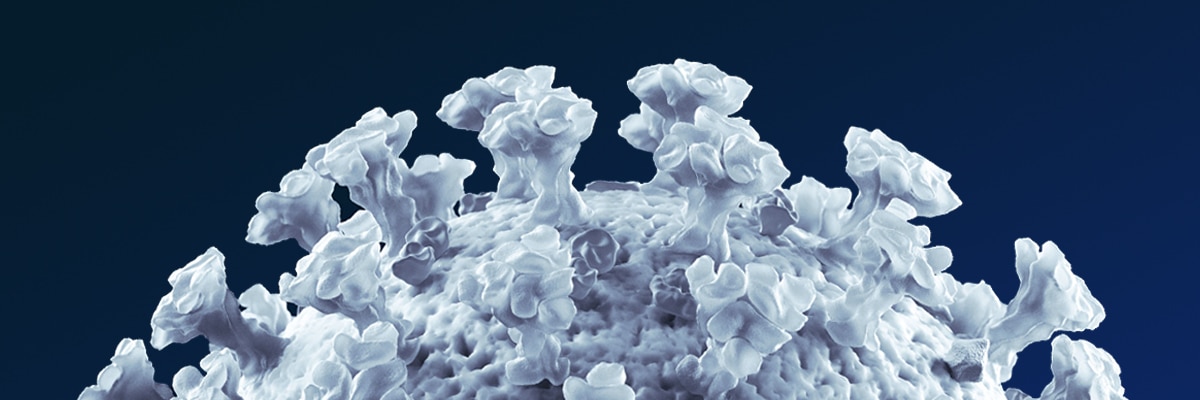

| The number of coronavirus cases is rising globally; travel bans and lockdowns are in effect; schools and universities are moving to remote learning. The virus outbreak is, first and foremost, a human tragedy affecting hundreds of thousands of people. It is also having a growing impact on the global economy. |

| There are several broad economic scenarios that could unfold, ranging from more optimistic to less so. Let’s take a look at the global-slowdown scenario, noting that our perspective may change because the outbreak is moving quickly. Check here for updates. |

| This scenario assumes that most countries wouldn’t be able to achieve the same rapid control that China managed. In Europe and the United States, transmission would be high but remain localized, partly because individuals, companies, and governments would take strong countermeasures (including closing schools and canceling public events). For the United States, the scenario assumes between 10,000 and 500,000 total cases, with one major epicenter, two or three smaller centers, and a “long tail” of towns with a handful or a few dozen cases. |

| The global-slowdown scenario would see some spread in Africa, India, and other densely populated areas, but the transmissibility of the virus would decline naturally with the Northern Hemisphere spring. There would also be large shifts in people’s daily behaviors, lasting six to eight weeks in towns and cities with active transmission and three to four weeks in neighboring towns. The resulting demand shock would cut global GDP growth for 2020 in half, to between 1.0 and 1.5 percent, and pull the global economy into a slowdown, though not a recession. |

| In this scenario, a global slowdown would affect small and midsize companies more acutely. Less developed economies would suffer more than advanced economies. And not all sectors would be equally affected in this scenario. Service sectors, including aviation, travel, and tourism, are likely to be hardest hit. |

| In consumer goods, the steep drop in consumer demand would likely mean delayed demand. This would have implications for the many consumer companies (and their suppliers) that operate on thin working-capital margins. But demand would return in May to June as concern about the virus diminishes. For most other sectors, the impact would primarily be a function of the drop in national and global GDP rather than a direct impact of changed behaviors. Oil and gas, for instance, would be adversely affected as oil prices would stay lower than expected until the third quarter of 2020. |

| The coronavirus crisis is a story with an unclear ending. The above is just one of the scenarios we’ve analyzed, and the situation evolves daily. What is clear is that the human impact is already profound—and companies have an imperative to act immediately to protect their employees, address business challenges and risks, and help mitigate the outbreak in whatever ways they can. |

| For more details from our COVID-19 research, updated through March 9, check here. |

|

|

|

|

|

| PODCAST |

| Making diversity matter |

| Progress on workplace diversity has been slow and patchy. In this podcast, Vivian Hunt, a McKinsey senior partner and a managing partner for the firm’s UK and Ireland offices, gets to the heart of the case for creating a diverse workforce. “We know there are multiple things great companies do well, but one thing that’s true for high-performing companies is better diversity,” she said. “We are not saying diversity drives good performance, but every high-performing company in every industry in every country tends to be more diverse than most of its peers. They have a skill set at managing diverse types of talent, and you know it matters, in the end, to performance.”

|

|

|

|

|

| MORE ON MCKINSEY.COM |

| The fashion industry: Ten top themes | In an uncertain global atmosphere, brands, retailers, and other fashion-industry players must act strategically to capitalize on digital opportunities, boost earnings, and address sustainability. |

| The case for greener telecom network | Operators’ energy costs keep rising, but efficiency measures and organizational change can lower them by 15 to 20 percent in a year, benefiting company profits and the environment. |

| Managing tech-transformation fallout | Companies may be pausing to digest what they have accomplished before undertaking further large-scale evolution of their technology organizations, a survey shows. |

|

|

|

|

|

| WHAT WE’RE WATCHING |

| Kevin Sneader |

| As McKinsey’s global managing partner, Kevin Sneader is a busy guy. But he has found time to answer questions in “Business in 60 Seconds,” a new weekly video out on Thursdays from GZERO Media. In the first three segments, Kevin discusses whether companies are thinking about climate change, what’s behind the shift from shareholders to stakeholders, and what 21st-century CEOs are thinking about. |

| “Are CEOs getting real about climate change?” |

| The answer is yes. One, the threat is increasing. We have a real sense of that from the data and statistics. Two, it’s systemic. It doesn’t just impact an action that one person can take; there’s a whole system that needs to change. Three, it’s regressive. Many are worried that the actions the world needs to take will hit hardest those least able to afford to pay. Four, it’s geographic—often in places where supply chains are also located. Five, there’s a growing understanding that this is dynamic; the nature of the threat keeps changing. |

| Faced with all that, how can a CEO not take action? And that’s why, for many, this is no longer something on the side. It’s integral to their business plans, and they’re spending real time on it. |

| “What is driving the shift from shareholders to stakeholders?” |

| There’s a growing awareness that while the inequality gap has closed between countries, it’s increased within countries. There’s also a move toward more regional—and even local—approaches, with all the impact that has on everyone in the supply chain. |

| Also, it’s hard for any CEO not to be aware of the breakdown in trust, not just between business and society but among many institutions in society more generally. And we have our part to play. Perhaps most important is technology—the way it’s shifting jobs, and the recognition that the workforce and how it operates are no longer going to be taken for granted. There really needs to be a different approach. |

| “What’s on the mind of 21st century CEO leaders?” |

| The first question is, what’s my mission, and how do I explain it to the world? Then, to whom are we accountable, and what’s the right time horizon in which to think about the investments we make and the returns we earn? |

| Who benefits from these actions? How do we think about the way in which benefits get shared, whether it’s compensation or the broader dividends that our company generates? How do I think about the way the workforce is being changed through technology and the implications for the benefits and employment that workers enjoy? As part of that, how do I think about inclusion? |

|

|

|

|

| BACKTALK |

| Have feedback or other ideas? We’d love to hear from you. |

|

|

|

|

|

Copyright © 2020 | McKinsey & Company, 3 World Trade Center, 175 Greenwich Street, New York, NY 10007

|

|

|

|