| This week, we look at the challenging environment in the United States as businesses move to restart. Plus, an interview with Kate Walsh, the CEO of Boston Medical Center, and Jason Wright, a McKinsey partner, answers questions on the wealth gap faced by African-American families. |

|

|

|

| Restarting economies in this new phase of the coronavirus pandemic has been difficult all over the globe. However, the already-fraught reopening in the United States has reached new levels of complexity and emotion as protests against police brutality erupt across the country. Many Americans are deeply uncertain about what comes next, despite a strong desire to resume normal life. |

| First, the challenges. Most state governors have allowed stay-at-home orders to expire, enabling local economies to begin reopening. Government and business leaders hope the activity will inject much-needed capital into a struggling economy in which 40 million Americans are already unemployed. |

| More pain ahead. The McKinsey Global Institute estimates that up to 57 million Americans hold jobs that are at risk for layoffs, furloughs, or reduced hours or pay. The most vulnerable employees already hold low-wage jobs; 86 percent of the most at-risk workers are paid less than $40,000 a year. Moreover, black Americans are among the hardest hit by COVID-19. McKinsey finds that African Americans are nearly twice as likely to live in counties disproportionately at risk for health and economic disruption. |

| Small businesses account for a disproportionate share of vulnerable jobs, with minority-owned small businesses particularly at risk. At the same time, these minority-owned enterprises are experimenting with new ways of working to ensure their employees’ safety, and offering monetary relief to employees and community members. This may give us a glimpse of how US businesses will adapt in the wake of COVID-19. |

| Creeping optimism? US consumer sentiment is mixed, with many indicating that some of their behavioral changes may stick in the long term, especially when it comes to their use of digital platforms, apps, and other web services. However, discretionary-spending intent is starting to rebound since we began our surveys, led by food and personal-care services. Consumers say they intend to increase online shopping for household essentials and entertainment, a shift that has been driven primarily by millennials and higher-income consumers. |

| The key is to inject confidence. Under high levels of uncertainty, business leaders find it extremely difficult to make reliable plans for investment. The objective now must be to crush uncertainty as soon as possible. To renew and refresh their connections to the people they serve, companies need to recognize what’s happening now, and respond by providing these three things. |

| The fine print. Many companies are running spreadsheets to see how many people spaced six feet apart will fit in an office, planning one-way paths through the workplace, and figuring out adaptations to restrooms, lunchrooms, and entrances. All of those are critical tasks, but they are not enough. What’s needed is a return “muscle”: an enterprise-wide ability to absorb uncertainty and incorporate lessons into the operating model quickly. |

| Digital and analytics are crucial. With its problem-solving and predictive prowess, analytics is becoming a modern-day sextant to navigate the COVID-19 crisis. Analytics can help tackle numerous urgent tasks facing businesses today. Despite all the bad news of late, organizations can meet an uncertain future with careful planning and a determined mindset. |

|

|

|

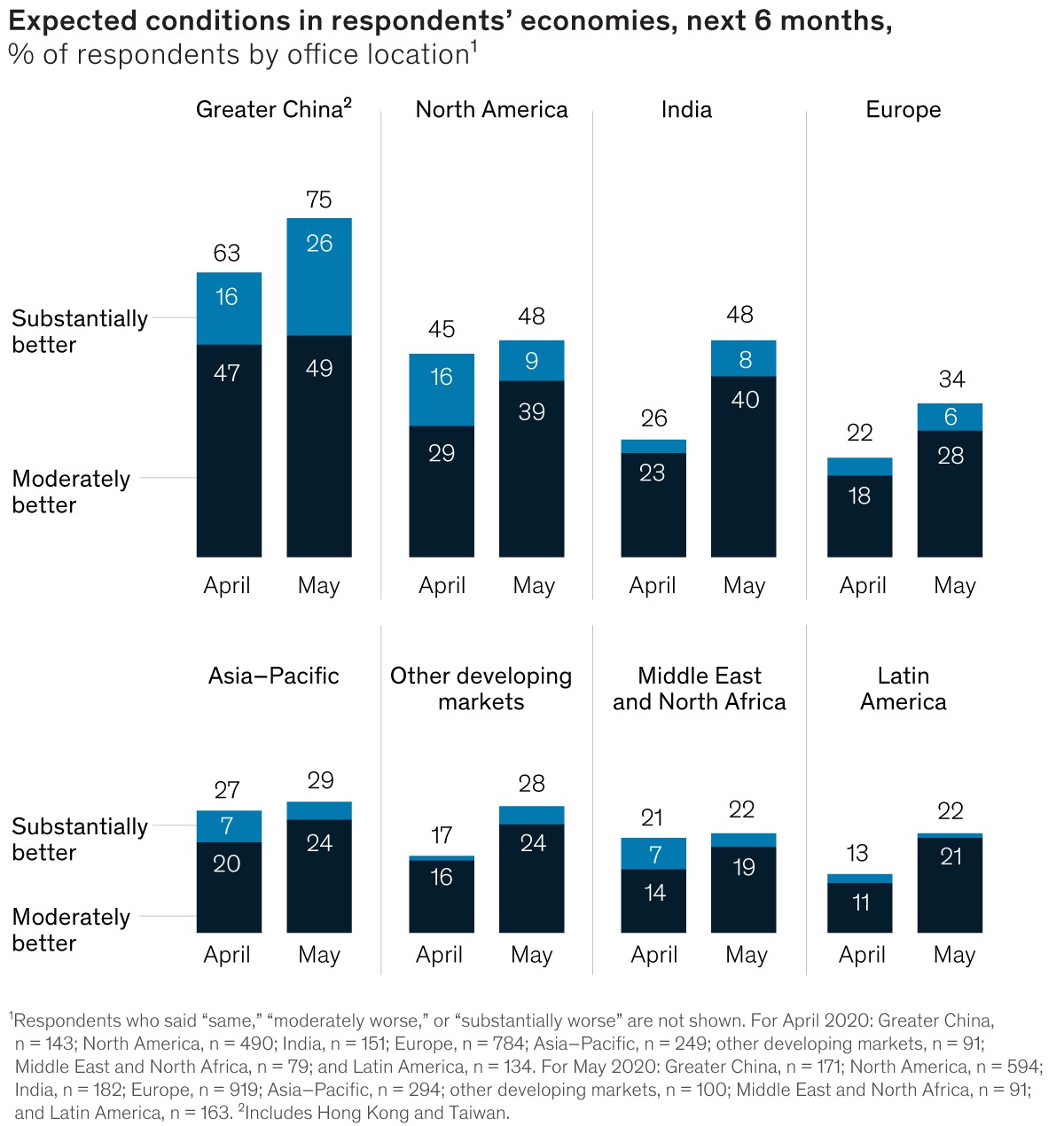

| OFF THE CHARTS |

| Global views paint a slightly brighter picture |

| Our May snapshot of executive sentiment shows that executives were much likelier than in April or March to expect improving conditions and increased growth rates in the months ahead, with respondents in Greater China the most optimistic of all. Yet most were still more negative than positive in their expectations for their home economies and the world economy at large. |

|

|

|

|

|

|

|

|

| INTERVIEW |

| ‘I’ve never seen anything like this’ |

| Urban hospitals in the United States have borne the brunt of the COVID-19 crisis so far, giving the leaders of these healthcare systems a valuable vantage point for the extreme measures required to respond effectively. Kate Walsh, the CEO of Boston Medical Center—the largest safety-net hospital in New England—was in the first wave of the response. In this video interview, Walsh discusses the challenges associated with treating vulnerable populations, the additional support required for employees, and how the pandemic could—and should—change healthcare. |

|

|

|

|

| MORE ON MCKINSEY.COM |

| Challenges for student learning in the United States | New evidence shows that the shutdowns caused by COVID-19 could exacerbate existing achievement gaps, which costs the United States hundreds of billions of dollars and exacts a long-term cost in social cohesion. This is a moment—and a challenge—that calls for urgency and energy. |

| A transformative moment for philanthropy | From the launch of community-based rapid-response funds to the development of diagnostics and vaccines, the philanthropic response to COVID-19 has shown the sector at its best. |

| What does the future hold for US restaurants? | How quickly will US consumers feel comfortable eating out again? We lay out potential timelines for the US restaurant industry’s recovery—and actions that restaurants should take to cater to consumers’ new dining needs and preferences. |

|

|

|

|

|

| THREE QUESTIONS FOR |

| Jason Wright |

| Jason Wright, a partner in McKinsey’s Washington, DC, office, focuses on modernizing higher-education institutions, government agencies, and industrial companies through large-scale transformations. Jason also co-leads McKinsey’s global inclusion strategy and spearheads global outreach to executives of color.

|

|

|

|

|

| African-American families still lag behind white families in terms of wealth. How can that change? |

| The wealth gap leaves many black families at a significant economic disadvantage, with less financial security and less ability to fully participate in the economy. Less wealth also means black Americans are underrepresented in the market for financial products and services. A lack of access to financial services is not just a symptom of the racial wealth gap; it is also a cause. Without the ability to affordably save, invest, and insure themselves against risks, many black families struggle to translate the income they earn into wealth. |

| Greater access to financial services could be central in closing the gap. We have identified five key aspects of financial inclusion. A household with full access to the financial system should be able to make everyday transactions through a safe and affordable transaction account, have access to credit, hold insurance against key risks, be able to save for big goals or rainy days, and ultimately accumulate long-term wealth. While many families take these elements of financial inclusion for granted, black families face more difficulties gaining access to the whole puzzle. |

| What are the challenges of being financially excluded? |

| Black families face greater geographic isolation, fewer products tailored to their economic realities, explicit racial discrimination and bias, and more. |

| Two simple factors tell the tale: banking and car ownership. Basic checking and savings accounts are harder for black consumers to open and more expensive for them to maintain. In majority-white counties, there are 41 banks per 100,000 people, compared with just 27 in neighborhoods where the majority are people of color. And when black families do gain access, they often pay more than their white counterparts. |

| Car ownership, too, is essential in many communities for getting to work and holding a job, but it is more expensive for the financially excluded. People of color are more likely to be offered costlier pricing options than their white counterparts. |

| Financial exclusion also has intergenerational consequences, creating real challenges in black families’ ability to sustainably build wealth. Moreover, modern-day financial disparities, such as the approximately 45 percent of black individuals who report experiencing racial discrimination when trying to rent an apartment or buy a home (compared with 5 percent of white Americans) continue to make economic mobility and wealth building more difficult for black Americans. |

| What changes can be taken to tangibly improve this picture for black families? |

| Financial inclusion will not be achieved unless the private, public, and social sectors commit to coordinated efforts. Leaders at banks and other private-sector institutions can make an enormous difference simply by rooting out the geographic, process, and economic barriers at their institutions that make it more difficult for black families to gain full access to financial products and services. |

| The public sector, in its role as policy maker, regulator, watchdog, and developer of financial infrastructure, could identify and support initiatives such as student-loan reform (black Americans with bachelor’s degrees who took out student loans hold nearly $4,400 more debt than the average American college graduate) and innovative systems that support multidimensional credit scoring. |

| In addition, the public sector could monitor and enforce equity in policies related to financial inclusion—for example, ensuring real-estate agents do not discriminate against black families who wish to move into neighborhoods that do not comprise majority black residents. The social sector, meanwhile, can help identify and pilot innovative solutions that, once proven, could be brought to scale. |

|

|

|

| BACKTALK |

| Have feedback or other ideas? We’d love to hear from you. |

|

|

|

|

|

Copyright © 2020 | McKinsey & Company, 3 World Trade Center, 175 Greenwich Street, New York, NY 10007

|

|

|

|